Investment institutions

The Netherlands as choice of your jurisdiction

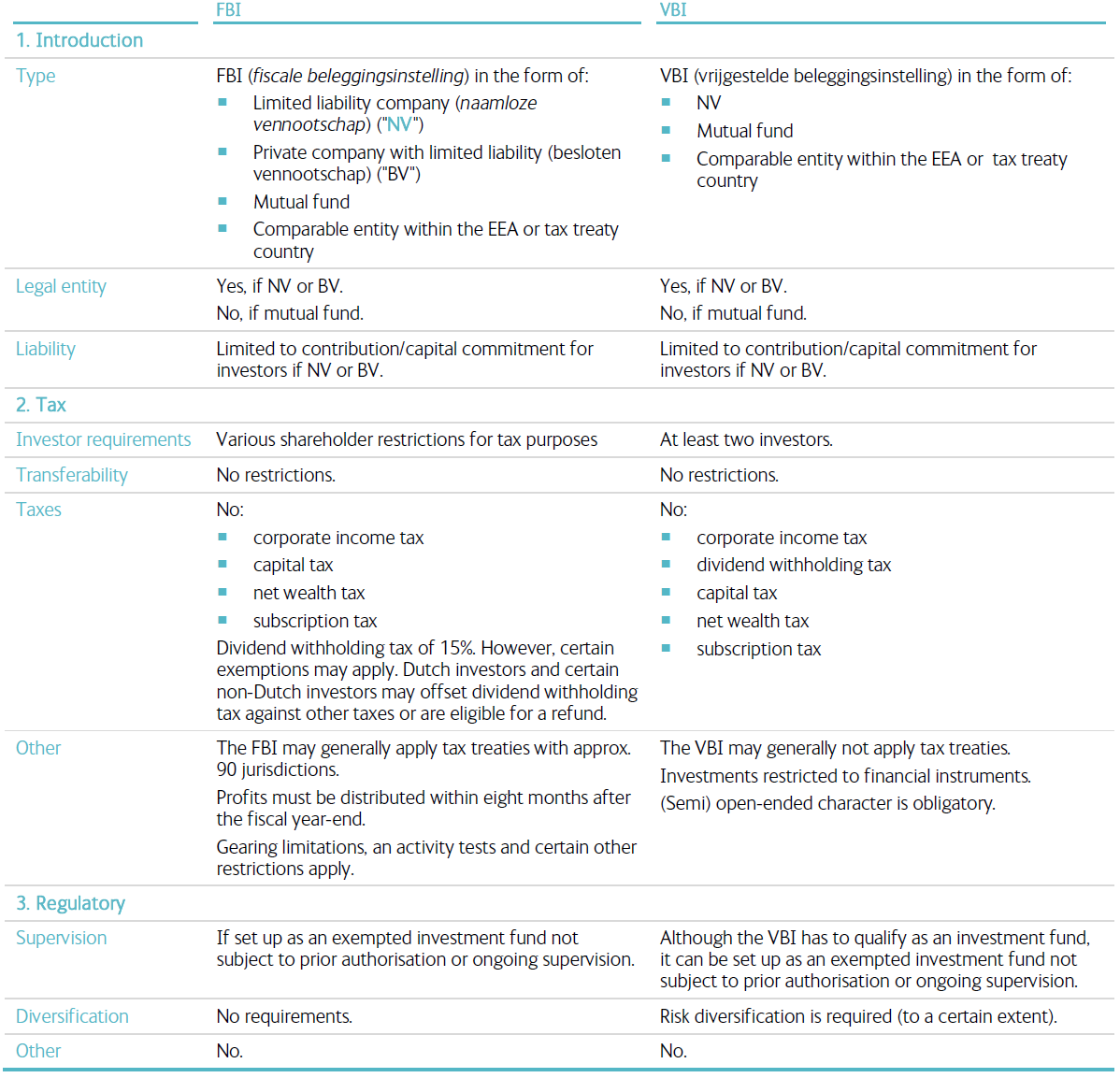

The Dutch tax system has many features that make the Netherlands a favourable jurisdiction for establishing an onshore investment institution. Examples include the absence of withholding tax on outbound interest and royalty payments, the absence of stamp duty and contribution capital tax and an extensive double tax treaty network. In addition, the Netherlands offers a number of alternative tax efficient fund regimes, such as the fiscal investment institution (fiscale beleggingsinstelling) (the “FBI”) and the fully tax exempt investment institution (vrijgestelde beleggingsinstelling) (the “VBI”) This VBI fund regime may be an attractive structure for all kinds of investments. The FBI is used by investment institutions which, among certain other areas, focus on investments in securities and real estate, (typically but not only) for tax exempt and retail investors. The VBI fund regime may be an attractive structure for all kinds of (passive) investments.

We believe that the Netherlands is a very attractive ‘on-shore gateway jurisdiction’ for international investment institutions.

1. Civil law aspects

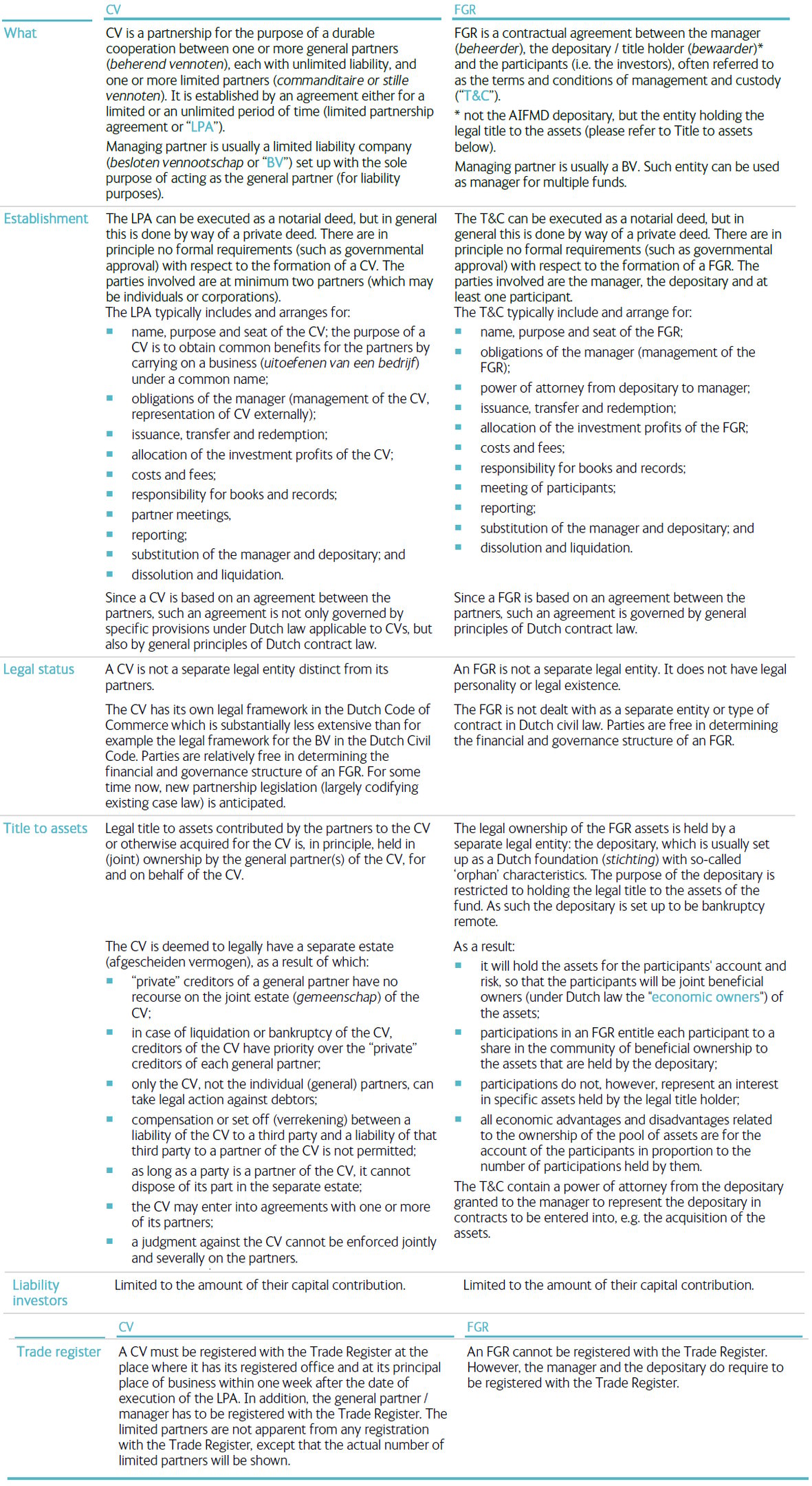

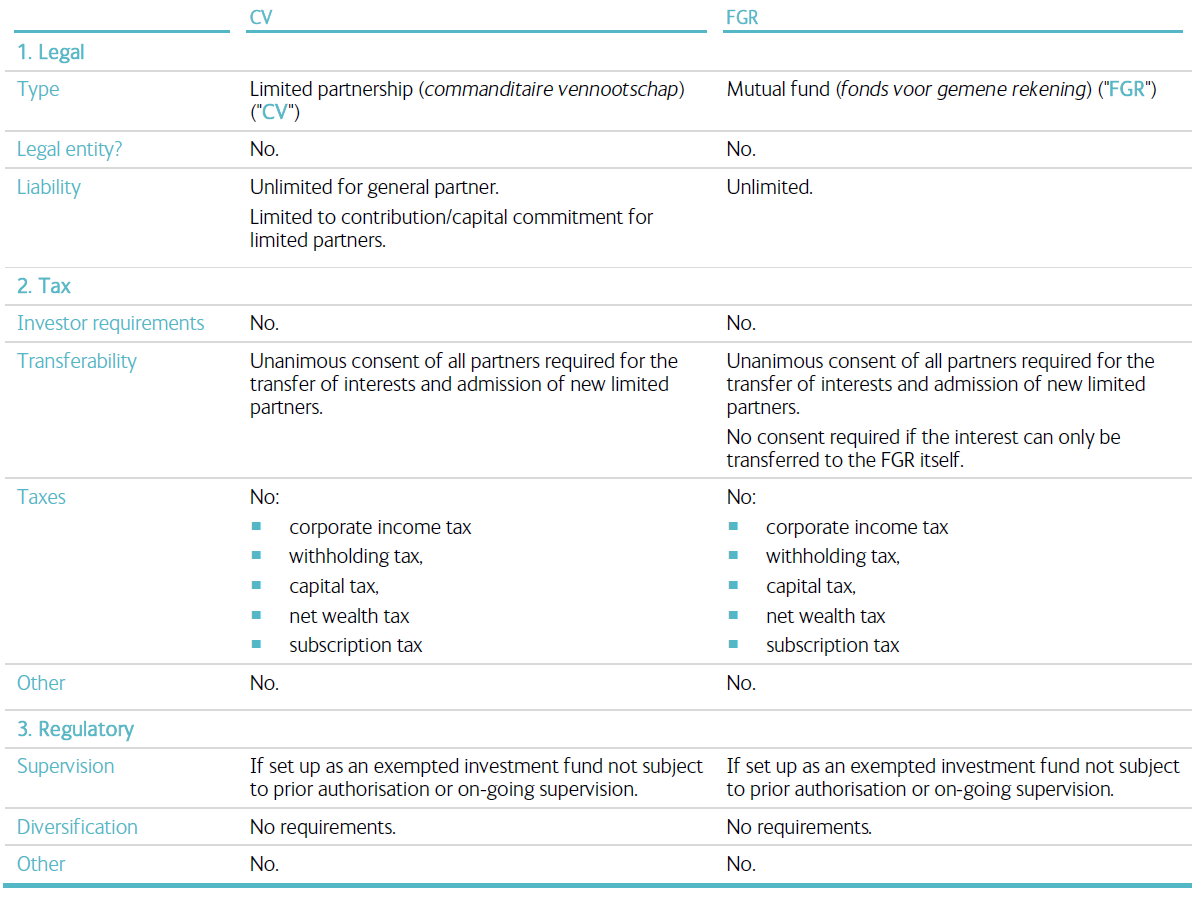

A Dutch limited partnership (commanditaire vennootschap or “CV”) or a mutual fund (fonds voor gemene rekening or “FGR”) are commonly used vehicles to structure an investment fund, mainly for creating optimal tax treatment for investors (as detailed under Tax Considerations below). As such investors are familiar with this concept and structuring wise it is a flexible option (as detailed below).

Main characteristics

2. Regulatory considerations

From a regulatory perspective, regulated investment funds in the Netherlands are either UCITS (icbe) or AIF (alternatieve beleggingsinstelling). The relevant European directives (AIFMD and UCITS V) have been implemented in the Dutch Financial Supervision Act (FSA).

Licensing requirement

An AIF manager (AIFM) is required to obtain a license in the Netherlands if:

it manages a Dutch AIF;

it offers participation rights in an AIF in the Netherlands; and/or

it is a Dutch manager and it manages an AIF or offers participation rights in an AIF.

A number of exemptions to the licensing requirement and/or alternative regimes are available for an AIFM in the Netherlands:

AuM below de-minimis thresholds: if (a) its overall assets do not exceed a certain threshold (ie AuM not more than (i) € 100 mio.; or (ii) € 500 mio if the funds do not use leverage and which have no redemption rights exercisable during a period of 5 years following the date of initial investment in each AIF) and (b) other conditions with regard to the investors or the marketed units are met. In that case the Dutch AIFM is only subject to registration with the AFM and reporting obligations to the Dutch Central Bank, which leads to lower costs.

Voluntary supervision: as, from a commercial perspective, it might be interesting for AIFMs to be subject to supervision. Therefore, the Dutch law provides an ‘opt-in’ possibility, which means that an AIFM may voluntarily apply for a license.

Non Dutch AIFMs: AIFMs which passport AIFs to the Netherlands (see below Passport) and AIFMs from equivalent third countries.

A UCITS manager is required to obtain a license in the Netherlands if it offers participation rights in a UCITS fund in the Netherlands. Other than passported (see below Passport) UCITS and UCITS from equivalent third countries there are no exemptions to this licensing obligation.

Application procedure

The procedure for application involves submission of a template application form including the required supporting documents to the AFM for review. Part of the application process is a test of suitability and reliability of the board members and supervisory board members of the AIFM (and potentially any other persons which qualify as a co-policymaker need to be tested for reliability). Additional forms must be provided along with the template application form, including: notification form for AIFs managed, a notification form for the AIFMD depositary and application forms for the suitability and reliability testing for each (supervisory) board member. The AFM may decide on a license application within as little as 13 weeks, however it may take a maximum period of 26 weeks. If the AFM foresees that it will take longer than 13 weeks to decide, it will inform the applicant thereof.

Passport

If a Dutch AIF or UCITS manager has a license from the Authority for the Financial Markets (AFM), it may use that license as well to market an AIF or UCITS in other EU member states and to manage an AIF or UCITS domiciled in other EU member states (“the European passport regime”).

Legal owner of fund assets

Pursuant to the FSA, if an AIFM or a UCITS manager sets up a fund without legal personality (such as a FGR) a ‘legal owner’ must be appointed to hold the assets of the relevant fund (this is in addition to the depositary required pursuant to the implementation of AIFMD and UCITS V).

We set out below some key considerations regarding the Netherlands as choice of jurisdiction for investment institutions. Also, we have included two matrices (for non-transparent and transparent structures). The matrices prove that the Netherlands is a major contender jurisdiction for investment institutions.

Benefits of choosing the Netherlands as jurisdiction for investment institutions include the following:

the Netherlands has a mature, suitable regulatory (also see below) regime adopting the relevant EU Directives;

the Netherlands has a short set up period as no waiting periods apply;

the professionals that investment funds usually deal with are very efficient and service minded. This does not only apply to advisors, such as lawyers, tax consultants and auditors, but also to the Dutch regulator and the Dutch tax authorities;

the Netherlands has a strong network of double taxation treaties (around 90 jurisdictions);

there is no relevant capital tax, stamp duty or similar documentary taxes.

3. Tax Considerations

Non-transparent

Main advantages of the FBI:

limited requirements with regard to the legal structure (company, contractual)

wide range of eligible investments

also foreign funds may qualify as FBI

various helpful exceptions to avoid licensing requirement for fund/its manager

no mandatory (local) custodian (only for Dutch, regulated contractual funds)

reduction of, or exemption from, withholding tax on investments made by the fund under double taxation treaties

subject to a 0% corporate income tax rate

Main advantages of the VBI:

limited requirements with regard to the legal structure (company, contractual)

eligible investments which comprise securities and participations in funds

also foreign funds may qualify as VBI

no leverage restrictions

various helpful exceptions to avoid licensing requirement for fund/its manager

no mandatory (local) custodian (only for Dutch, regulated contractual funds)

exempt from corporate income tax and withholding tax on distributions to participants in the fund

Non-transparent

Main advantages of the CV and the FGR:

limited liability for limited partners

not subject to corporate income tax, withholding tax, capital tax, net wealth tax and subscription tax

4. Conclusion

The FBI is widely used as an investment fund for investments in securities and real estate, as the FBI may claim tax treaty benefits, for example on dividend received by the FBI.

The VBI does not impose an additional tax burden at the level of the fund nor on the level of the investor. As a result, the VBI will continue within the track record set by the FBI further aiming to deliver a tailor made on-shore investment fund regime in a way that compares favorably with other international off shore funds.

Both the CV and the FGR do not impose an additional tax burden at the level of the fund.

Non tax transparent funds

Tax transparent funds

FIDELIS ONE ADVISORS

Paseo de los Tamarindos 400B,

Bosques de las Lomas, 05120ZP

Mexico City

_______________________________________

Haringvliet 461

3011 ZP Rotterdam

The Netherlands

+525567875311

info@fidelisoneadvisors.com