Structuring of a fund (the Netherlands, Luxembourg, Ireland, the Cayman Islands and Switzerland)

3.1 Legal structures Dutch funds

A well-known vehicle used by both private individuals and corporations is the Dutch fund for joint account (besloten fonds voor gemene rekening). This type of fund is often used in situations when admission of new investors and redemptions of participations will take place on a regular basis, as a result of which other possible Dutch vehicles are less usable. Properly structured, such fund will be transparent for tax purposes in the Netherlands, which means that no corporate income tax is levied at fund level. Taxes will only be levied at the level of the investors. This type of fund is often the best option when looking for a tax-transparent fund entity that is not located in a blacklisted jurisdiction and can facilitate investments by multiple unrelated investors. In addition, treaty benefits can be obtained for the underlying investors when required.

The fund for joint account does not have legal personality. Usually the assets of the fund are held by a custodian and fund management will be the responsibility of a separate manager. In case the fund is structured as non-tax transparent, it may benefit from the preferential tax treatment of the fiscal investment company (as described in paragraph 3.2).

Fund for joint account (besloten fonds voor gemene rekening)

Next to Fund for joint accounts, the Netherlands has the regular legal structures in place such as a NV, BV, Co-operative and a limited partnership (CV). Tax structures as defined below can be structured in one of these legal corporate entities.

Corporate entities

3.2 Tax structures Dutch funds

Fiscal investment company (fiscale beleggingsinstelling)

Portfolio investment income received by an entity (a BV, NV, non-tax transparent fund for joint account, or comparable foreign entities) that has obtained the status of fiscal investment company (fiscale beleggingsinstelling, FBI) can qualify for a 0% corporate income tax rate. In order to qualify for this regime certain conditions are to be met with regard to amongst others the shareholders, the activities, the funding and the distributions of profits. Another benefit of the FBI is that despite the applicable 0% tax rate, the Dutch tax authorities take the position that such company is subject to tax and as such it should qualify for the benefits provided for by the Dutch tax treaties (i.e. reduced withholding tax rates).

Tax-exempt investment company (vrijgestelde beleggingsinstelling)

As from 1 August 2007, a special regime is introduced for portfolio investment companies. Under certain conditions an NV, fonds voor gemene rekening or a comparable foreign entity whose main activity consists of managing portfolio investments on behalf of its shareholders, may opt for full exemption of Dutch corporate income tax and dividend withholding tax. This exempt NV is referred to as a tax-exempt investment company (vrijgestelde beleggingsinstelling, VBI).

A VBI should meet certain risk diversification measures that apply and eligible investments are, amongst others, marketable shares and bonds, instruments commonly traded on the money markets, commodity derivatives, forward contracts, swaps, and options of the aforementioned instruments. Under the VBI regime it is not possible to invest directly in real estate; however, it may be possible to invest in shares of a company owning real estate.

However, the VBI will not be considered resident in the Netherlands for double tax treaty purposes. As such it will not be possible to reclaim foreign withholding tax on dividends or interest under relevant double tax agreements.

Unlike the FBI regime there are no shareholder requirements, financing limits or distribution obligations.

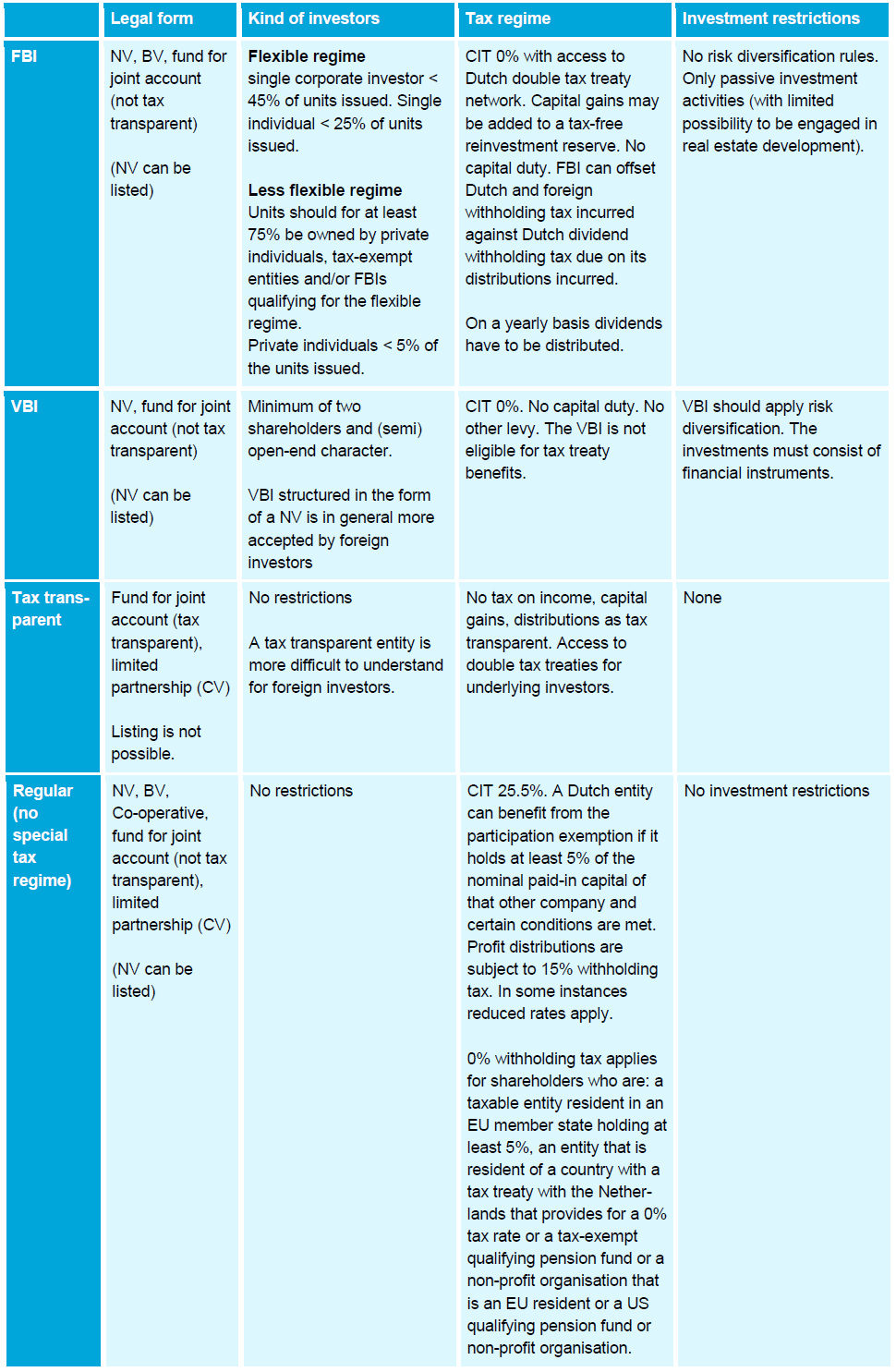

3.3 Overview of the four structures (FBI, VBI, tax transparent and corporate entities)

An overview of the key characteristics of the structures described is as follows:

3.4 Legal structures Luxembourg funds

Luxembourg investment funds

Luxembourg investment funds are either created under a contractual or a corporate form. The contractual form is the so-called Fonds Commun de Placement (FCP) and the corporate form the so-called Investment Company with Variable Capital (SICAV).

The FCP is an undivided collection of assets, managed by a management company on behalf of joint owners („the unit holders‟). Legally speaking it is established by a contract between the management company and the custodian bank, which creates management regulations. Investors in the form of unit holders, buy units issued by the management company, which represent a portion of the FCP managed, and by doing so become a party to the contract. The units acquired represent their right in the undivided collection of assets. Their liability is limited to the amount they contributed.

SICAVs are corporate vehicles whose articles of incorporation provide that the amount of capital is at all times equal to the net asset value (NAV) of the vehicle. As a result of subscriptions or redemptions the capital increases or decreases automatically, without any of the formalities generally imposed under Luxembourg company law regarding issuance or reduction of capital. SICAV investors are shareholders and as such have a right to vote in shareholders‟ meetings in addition to their economic rights. SICAVs may take different legal forms: as a limited company (S.A.), in accordance with the Specialised Investment Funds (SIV) laws, as a limited partnership (S.C.A.), or as a private limited company (S.à r.l.).

Luxembourg private equity and venture capital funds

As of June 2004 Luxembourg has created a Société d’investissement en capital a risqué (SICAR). SICARs are technically not investment funds, but resemble their functioning closely. SICARs are exclusively reserved for well-informed investors and are, apart from the SIFs, the prime vehicles for investing into private equity and venture capital.

The limited partnership (société en commandite simple or SCS) is the risk capital vehicle under the SICAR regime.

3.5 Legal structures Irish funds

Irish structures

Ireland has three types of funds (in addition to UCIT funds)

1. a unit trust authorised under the Unit Trust Act 1990;

2. an investment company registered as a public limited company under Part XIII of the Companies Act 1990;

3. an investment limited partnership authorised under the Investment Limited Partnership Act 1994.

Unit trust

A unit trust operates as an investment fund established under a trust deed made between (i) the management company and (ii) the trustee. The trustee acts as the legal owner of the fund‟s assets on behalf of the investors who are each entitled to an undivided beneficial interest in the fund. Similar to shareholders in an investment company the unit holders are entitled to attend and vote at meetings on matters affecting the fund.

The trust deed is the primary legal document which constitutes the trust and it sets out the various rights and obligations of the trustee, the management company and the unit holders. The trust deed will usually delegate the day-to-day management of the unit trust to the management company that usually delegates these functions to third-party service providers.

Variable capital company

Companies are registered under a series of acts called the Companies Acts 1963 to 1999. The shareholders of the company enjoy limited liability. The main aim of funds set up as investment companies is the collective investment of its funds and property with the aim of spreading investment risk. A company is managed for the benefit of its shareholders. Variable capital companies can repurchase their own shares and their issued share capital must at all times be equal to the net asset value of the underlying assets. Irish companies must have a minimum of two Irish directors.

The investment limited partnership fund structure was introduced in Ireland in July 1994 under the Investment Limited Partnerships Act, 1994. An investment limited partnership is a partnership of two or more persons, having as its principal business the investment of its funds in all kinds of property and consisting of at least one general partner and at least one limited partnership. The limited partner is equivalent to the shareholder in a company while the general partner would be the equivalent of the management company in a unit trust. The main advantage of a limited partnership is that the partnership does not have an independent legal existence in the way that a company does. All of the assets and liabilities belong jointly to the individual partners in the proportions agreed in the partnership deed. Similarly, the profits are owned by the partners. This structure may have some tax benefits associated with it. Each partner is entitled to use any tax reliefs and allowances the partnership is entitled to as agreed between each partner, subject to any tax rules governing the allocation of the reliefs and allowances.

Apart from these three legal structures a common contractual fund may be established.

Investment limited partnership

Common contractual fund (CCF)

A CCF is a contractual arrangement established under a deed, which provides that investors participate as co-owners of the assets of the fund. The ownership interests of investors are represented by „units‟, which are issued and redeemed in a manner similar to a unit trust.

The CCF is an unincorporated body, not a separate legal entity and is transparent for Irish legal and tax purposes. As a result, investors in a CCF are treated as if they directly own a proportionate share of the underlying investments of the CCF rather than shares or units in an entity which itself owns the underlying investments.

A CCF can be established as a UCITS fund or a non-UCITS fund. Tax transparency is the main feature, which differentiates the CCF from other types of Irish funds. The CCF is authorised and regulated by the Irish Financial Regulator.

Qualified investor fund (QIF)

All of the Financial Regulator‟s investment and borrowing restrictions are automatically derogated from for a QIF. To qualify as a QIF, the minimum subscription is EUR 250,000. In addition the investor must be either:

a person with a minimum net worth in excess of EUR 1,250,000, excluding main residence and household goods; or

an institution (a) which owns or invests on a discretionary basis at least EUR 25 million or its equivalent in other currencies or (b) the beneficial owners of which are qualifying investors in their own right.

The qualifying investor is required to certify itself as such on the application form for investment in the fund.

3.6 Legal structures Cayman Islands funds

The four vehicles commonly used for operating mutual funds are the exempted company, the segregated portfolio company, the unit trust and the exempted limited partnership.

Exempted company

The exempted company may redeem or purchase its own shares and may therefore operate as an open-end corporate fund. Closed-end corporate funds can also be established using the exempted company and it is a relatively straightforward procedure to convert from one to the other.

Segregated portfolio company

An exempted company can also be established as a segregated portfolio company (SPC) with protected cells or portfolios. The SPC makes it possible to provide a means for different groups to protect their assets when carrying on business through a single legal entity.

Unit trust

The unit trust is usually established under a trust deed with the investors‟ interest held as trust units.

Exempted limited partnership

The exempted limited partnership provides a second unincorporated vehicle and it can be formed as easily as the exempted company or the unit trust.

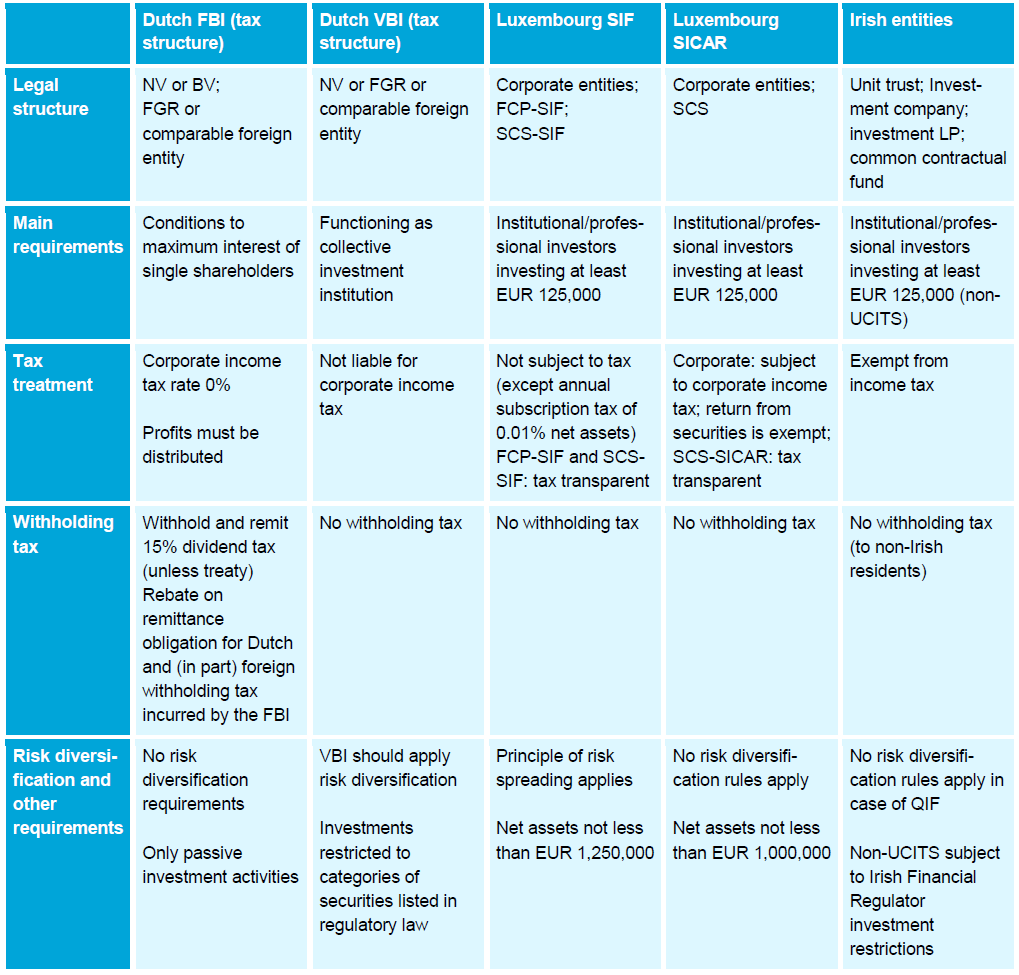

3.7 Dutch structures compared to Luxembourg and Irish structures

An overview of Dutch structures compared to Luxembourg and Irish structures is as follows:

Based on the above we conclude that a Dutch structure is as competitive or even more so than Luxembourg or Irish fund structures. If your fund has a significant dividend income stream from its underlying investments, the Dutch FGR structure is even „best in class‟, as it will enable you to benefit from the Dutch tax treaties in respect of withholding taxes.

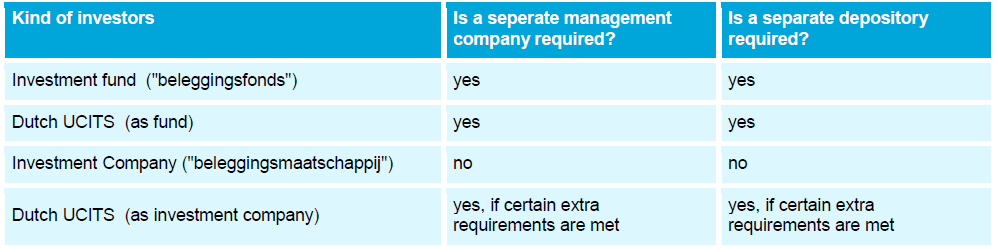

3.8 Depository System in the Netherlands.

A separate depository as well as a separate management company is required for investment funds (“beleggingsfonds”) and UCITS funds (as a unit trust). For investment companies (“beleggingsmaatschappij”) a separate management company and depository are not mandatory (see the table below). A depository acquires and administers assets for the benefit of the unit holders and can access the assets with the cooperation of the management company. The management company and the depository need to conclude a written management and custody agreement. There are certain minimum requirements for these agreements which have to be met. Furthermore, it is not required that the registered office is in the Netherlands and there are no requirements regarding the legal form. The foundation (“stichting”) is the most preferred legal form by far.

FIDELIS ONE ADVISORS

Paseo de los Tamarindos 400B,

Bosques de las Lomas, 05120ZP

Mexico City

_______________________________________

Haringvliet 461

3011 ZP Rotterdam

The Netherlands

+525567875311

info@fidelisoneadvisors.com